Price: $9.99 (as of Jan 23,2025 04:40:21 UTC – Details)

Buy a brand you can trust. Choose UpStart Battery. Product Specifications Chemistry: Li-Ion Output Volts: 3.6V Capacity: 680mAh Color: Black / UpStart Logo Warranty: Lifetime Warranty Package: Retail Blister Pack 100-240V autosensing for world wide use CE and UL Approved Overcharge prevention circuitry Lifetime Warranty Brand: UpStart Battery This Product works in or replaces the following OEM model numbers: CANON

NB-11L

CB-2LD

IXUS 125 HS

IXUS 240 HS

IXY 220F

IXY 420F

PowerShot A2300

PowerShot A2400 IS

PowerShot A3400 IS

PowerShot A4000 IS

PowerShot ELPH 110 HS

PowerShot ELPH 320 HS

Premium Quality, Lifetime Warranty CE Approved and Safety Assured Output Volts: 3.6V, Capacity: 680mAh Color: Black / UpStart Logo Brand: UpStart Battery

Looking for a reliable and affordable battery and charger kit for your Canon digital camera? Look no further than the Upstart Battery NB-11L Replacement Battery and Charger Kit!

This kit includes a high-quality replacement battery for the Canon NB-11L, as well as a convenient charger that allows you to easily charge your battery wherever you go. With a capacity of 900mAh, this battery provides long-lasting power for all your photography needs.

Whether you’re a professional photographer or just a casual shooter, having a reliable battery is essential for capturing those perfect moments. Don’t let a dead battery ruin your shot – invest in the Upstart Battery NB-11L Replacement Battery and Charger Kit today!

Compatible with a wide range of Canon digital cameras, this kit is a must-have for any photographer. Say goodbye to constantly buying disposable batteries and switch to a rechargeable option that will save you time and money in the long run.

Don’t miss out on this great deal – order your Upstart Battery NB-11L Replacement Battery and Charger Kit now and never miss a shot again!

#Upstart #Battery #NB11L #Replacement #Battery #Charger #Kit #Canon #Digital #Cameras #Brand,canon ixy 420f

Shares of Upstart Holdings Inc (UPST, Financial) fell 6.43% in mid-day trading on Dec 27. The stock reached an intraday low of $67.26, before recovering slightly to $67.40, down from its previous close of $72.03. This places UPST 24.23% below its 52-week high of $88.95 and 227.18% above its 52-week low of $20.60. Trading volume was 1,954,792 shares, 25.4% of the average daily volume of 7,691,213.

Wall Street Analysts Forecast

Based on the one-year price targets offered by 15 analysts, the average target price for Upstart Holdings Inc (UPST, Financial) is $57.17 with a high estimate of $100.00 and a low estimate of $9.00. The average target implies an downside of 15.18% from the current price of $67.40. More detailed estimate data can be found on the Upstart Holdings Inc (UPST) Forecast page.

Based on the consensus recommendation from 16 brokerage firms, Upstart Holdings Inc’s (UPST, Financial) average brokerage recommendation is currently 3.0, indicating “Hold” status. The rating scale ranges from 1 to 5, where 1 signifies Strong Buy, and 5 denotes Sell.

Based on GuruFocus estimates, the estimated GF Value for Upstart Holdings Inc (UPST, Financial) in one year is $37.54, suggesting a downside of 44.3% from the current price of $67.4. GF Value is GuruFocus’ estimate of the fair value that the stock should be traded at. It is calculated based on the historical multiples the stock has traded at previously, as well as past business growth and the future estimates of the business’ performance. More detailed data can be found on the Upstart Holdings Inc (UPST) Summary page.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.

On December 27, shares of Upstart Holdings Inc (UPST) saw a significant decrease, dropping 6.43% in value. This decline comes after a period of strong growth for the company, which has been making waves in the financial technology industry.

Investors may be reacting to various factors such as market volatility, profit-taking, or broader economic concerns. It’s important to note that one day of trading does not necessarily indicate a long-term trend, and fluctuations in stock prices are common in the market.

Despite this recent dip, Upstart Holdings Inc remains a promising player in the fintech sector, with its innovative AI-driven lending platform disrupting traditional lending practices. Investors and analysts will be closely watching to see how the company performs in the coming days and weeks.

Upstart Holdings’ stock has enjoyed a scintillating run in its past six months, surging by approximately 260%. However, despite its astounding form, the sustainability of Upstart’s latest surge can be contested by talks of re-inflation, a potential shift in credit risk, and Upstart’s ongoing profitability concerns.

Aside from the above-mentioned, JP Morgan recently downgraded Upstart to ‘underweight’ on the basis of an unjustified valuation. According to JP Morgan, Upstart’s “shares seem to be priced to perfection,” adding substance to a revision of the stock’s prospects.

The headwinds mentioned within the introduction provide a summary; let’s traverse into a more comprehensive discussion of Upstart’s emerging headwinds.

Critiquing Upstart requires an understanding of its business model. For those unaware, Upstart is a lending marketplace that leverages artificial intelligence to curate comprehensive borrower credit scores. The company passes its data analytics to banks, who ultimately write consumer loans.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Upstart

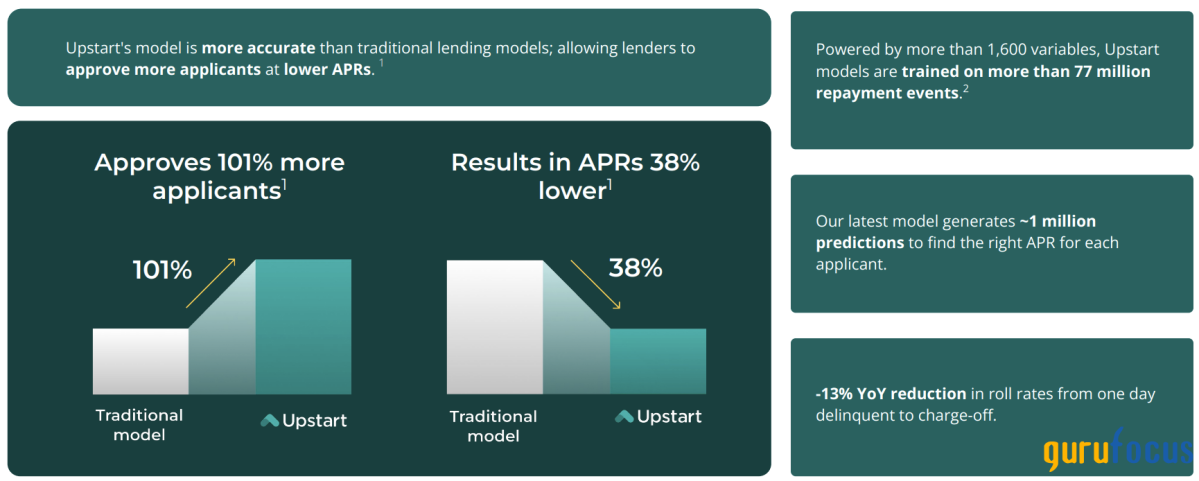

Upstart’s business model has delivered tangible success as the company’s loan approval rate outpaces that of traditional banks while also reducing the borrower’s repayment rate. Moreover, Upstart has successfully implemented a complex model, where it bases its scenario analysis on over 1,600 variables and 77 million repayment events, illustrating the company’s successful use of big data analytics to curate justified credit scores.

Another compelling feature of Upstart is its ‘skin in the game,’ whereby the company holds its very own loan portfolio, showing its commitment to its methodology. As illustrated in the following diagram, Upstart recorded approximately $334 million in co-investments during its latest quarter, a substantial increase from $66 million a year prior.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Upstart

Upstart’s identifiable key drivers are both internal and external.

Firstly, as previously mentioned, the company utilizes a comprehensive screening methodology whereby it leverages artificial intelligence to optimize large data sets. Moreover, its machine learning techniques incorporate non-linear relationships, allowing Upstart to generate a wider breadth of scenarios than traditional economic models otherwise would.

Upstart’s digitalization has evidently resulted in a cutting-edge marketplace. However, the company’s internal drivers are influenced by external factors such as interest rates, inflation, credit risk, and related variables. Therefore, a secondary driver for Upstart is the overall health of the lending environment.

Cumulatively, Upstart’s key drivers have contributed to its cyclical performance, displayed by the fact that the stock remains nearly $300 below the heights it achieved in 2021 when it reached the $380 handle.

An observation of Upstart’s stock price shows its correlation to interest rates. For example, the stock regressed since 2022’s rate hike cycle started, yet recovered when certainty of an interest rate pivot occurred earlier this year.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Yahoo Finance

The main reason for Upstart’s sensitivity to interest rates derives from its dependency on loan volumes. The company’s marketplace platform relies on fee-based earning and, therefore, acts counter-cyclically to interest rate levels.

Lower interest rates visibly spiked Upstart’s stock price since mid-year. However, disinflation has slowed, reducing the capacity for interest rate cuts. In fact, factors such as President Trump’s proposed tariffs, China’s stimulus, enhanced consumer sentiment, Middle Eastern tensions’ influence on oil prices, and enhanced industrial production might contribute to an argument for a 2025 re-inflation scenario.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Trading Economics

Whether effective rates decline in the coming quarters remains to be seen. Nonetheless, key variables suggest that investors might’ve overestimated the velocity of future disinflation, which, in turn, caused Upstart’s stock to surge beyond its fair value.

This sub-section’s title refers to the fact that Upstart’s advanced data analysis likely won’t defend against severe macroeconomic headwinds. The company’s methodology might produce relative value. However, a rapid rise in credit risk will ultimately reduce lenders’ willingness to write high-risk loans.

Credit spreads remain tight, suggesting the U.S. credit market is healthy. However, spreads are cyclical and mean-reverting; therefore, widening will likely occur at some stage. Upstart’s marketplace and loan book has flourished in 2024’s low-spread environment. Nevertheless, as mentioned, widening may disrupt its flow.

Why Upstart Might’ve Reached Its Peak, For Now

Source: St. Louis Federal Reserve

The question now becomes, what may cause spreads to widen again? A key driving factor could be consumer loan delinquencies. Delinquencies remain elevated, and lower U.S. interest rates haven’t decreased delinquencies by a material level. Thus, an argument exists that the real economy’s credit risk might be underpriced by spreads, causing investors to ramp up Upstart’s stock in recent months.

Why Upstart Might’ve Reached Its Peak, For Now

Source: St. Louis Federal Reserve

As with interest rates, 2025’s credit risk outlook is up for discussion. However, a decaying credit environment would likely dent Upstart’s loan origination volumes through lower conviction from banks and other lenders. Moreover, a secondary impact can occur as the company has consumer debt on its own balance sheet, with auto loans spanning most of Upstart’s loan book.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Upstart

Upstart’s business has scaled since its inception yet struggled to achieve profitability. Although running at a loss is normal for growth-stage firms, the nature of Upstart’s expenses conveys how expensive it is to expand its business model.

The following figure shows Upstart’s comprehensive income statement; a discussion follows.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Upstart

A telling feature of the company’s income statement is its engineering and product development line item, which spans approximately 32% of the company’s operating costs. While innovation is key, engineering costs can be persistent as top talent usually costs a premium. Upstart’s competitive advantage is product-driven; therefore, retaining top-tier engineering capabilities will be vital in the years ahead.

Furthermore, Upstart’s sales and marketing expenses comprise about 20% of the company’s expense base, while general and administrative expenses span roughly 29%. These costs are more straightforward to dilute than engineering expenses, especially if broad-based inflation stabilizes; however, a competitive environment poses challenges, likely forcing Upstart to inflate its marketing budget.

In effect, Upstart has a scalable business model. However, the competitive environment and Upstart’s product-centric approach mean Upstart’s top-line success is expensive to ascertain.

As pointed out earlier, JP Morgan is concerned about Upstart’s valuation outlook. Key metrics agree with the investment bank’s consensus. For example, Upstart’s price-to-sales ratio has nearly doubled since last year. Moreover, the company’s price-to-book ratio has surged to 11.78x from roughly 5.55x a year ago, while its price-to-free cash flow ratio is arguably outlying at 86.87x.

Why Upstart Might’ve Reached Its Peak, For Now

Source: Macro Trends

An isolated view of the Upstart’s price multiples accompanies the thesis’ fundamental argument. It is unlikely that Upstart’s fundamental growth will sustain its current multiples, especially if investors decide to ‘take profit.’

Lastly, Upstart had a 14-day relative strength index of 66 at the time of writing the article. For those unaware, an RSI of 70 and above suggests a stock is technically overbought. Therefore, Upstart’s RSI will likely cause concern in light of its elevated fundamental price multiples.

Upstart Holdings is a growing company with a highly compelling business model emphasizing a product-driven approach. However, history has proven that Upstart’s stock is cyclical, and key identifiers suggest that Upstart stock’s latest form might come to a halt in 2025.

While some might disagree with the fundamental argument, Upstart’s valuation multiples and technical features are hard to pass, even in a bull market.

Upstart’s stock seems overcooked for the time being.

Upstart has been gaining a lot of attention in the fintech world recently, with its innovative approach to lending and use of artificial intelligence to assess creditworthiness. However, there are some signs that the company may have reached its peak, at least for the time being.

One reason for this is the increasing competition in the fintech space. Upstart’s success has attracted a number of new players to the market, all vying for a piece of the pie. This increased competition could make it harder for Upstart to continue growing at the same rapid pace it has been.

Another factor to consider is the overall economic climate. With interest rates rising and the possibility of an economic downturn looming, consumers may become more cautious about taking on new debt. This could impact Upstart’s loan volumes and profitability.

Additionally, there have been some concerns raised about Upstart’s business model. Critics have questioned the accuracy of the company’s AI-driven credit assessments and raised concerns about potential bias in the algorithms. These issues could lead to regulatory scrutiny and damage Upstart’s reputation.

While Upstart has been a standout in the fintech world, it’s important to consider these potential challenges and monitor how the company navigates them in the coming months. It’s possible that Upstart will continue to thrive, but it’s also worth being cautious about its future prospects.

HANOI, VIETNAM – Media OutReach Newswire – 27 December 2024 – The VinFast VF 8 is produced at one of Southeast Asia’s most advanced manufacturing facilities, reflecting the Nasdaq-listed company’s focus on efficiency and innovation to meet the evolving needs of global consumers while contributing to a greener automotive future.

The VF 8 offers one of the most competitive lease deals in the U.S., easing the transition for those switching to electric vehicles.

Inside VinFast’s Haiphong factory, the VF 8 and other vehicles in their comprehensive EV lineup embody the company’s pioneering vision. Recognized for its innovation and speed to market, VinFast secured a spot on TIME’s 2024 list of influential companies. As VinFast expands globally, its vehicles demonstrate advanced engineering and a commitment to sustainability. Among these, the VF 8 emerges as a flagship model, offering a glimpse into a smarter and greener automotive future.

Designed for North America’s SUV-Loving Families

In North America, SUVs account for nearly 55% of all passenger vehicle sales in 2023[1], reflecting their enduring popularity. The VF 8 embraces this trend, combining an elegant SUV-coupe silhouette with practical features tailored for everyday use. Its sloping roofline maximizes style and interior space, making it a strong contender for families seeking both comfort and aesthetics.

The VF 8’s minimalistic interior design reduces physical buttons, enhancing driver focus while maintaining a modern, uncluttered look. Its spacious cabin ensures a comfortable experience for both short trips and long journeys. Powered by an electric drivetrain, the VF 8 boasts significantly lower operating costs than traditional ICE vehicles in the same segment. This efficiency is a key factor for families considering long-term savings.

Adding to its appeal, the VF 8 offers one of the most competitive lease deals in the U.S., easing the transition for those switching to electric vehicles.

The VF 8 embodies a commitment to innovation and sustainability, symbolizing Vietnam’s drive to lead the global green transformation.

The VF 8: A Testament to VinFast’s Vision

The VF 8 represents a milestone for VinFast, Vingroup, and Vietnam’s automotive ambitions. As Vietnam’s top car brand for the first 10 months of 2024, VinFast continues its global expansion with ventures in Indonesia, the Philippines, and the Middle East, as well as new assembly plants in Indonesia and India.

For Vingroup, the VF 8 embodies a commitment to innovation and sustainability, symbolizing Vietnam’s drive to lead the global green transformation. More than just a vehicle, the VF 8 showcases how thoughtful design and purpose-driven engineering can shape a better future.

Hashtag: #VinFast

The issuer is solely responsible for the content of this announcement.

News Source: VinFast

27/12/2024 Dissemination of a Financial Press Release, transmitted by EQS News. The issuer is solely responsible for the content of this announcement.

VinFast, the Vietnamese automotive company, is making waves in the industry with its latest announcement of the VinFast VF 8. This new vehicle showcases the upstart carmaker’s ambition and determination to succeed in the competitive automotive market.

The VinFast VF 8 is a sleek and stylish SUV that combines cutting-edge technology with luxurious design elements. With its powerful engine, advanced safety features, and spacious interior, the VF 8 is set to make a splash in the SUV segment.

VinFast has been making a name for itself in the automotive world with its innovative approach to design and manufacturing. The company’s commitment to quality and customer satisfaction has earned it a loyal following of customers who appreciate its attention to detail and commitment to excellence.

With the introduction of the VinFast VF 8, the company is poised to take its place among the top automotive manufacturers in the world. The VF 8 demonstrates VinFast’s dedication to pushing the boundaries of what is possible in the automotive industry and its determination to succeed against all odds.

Stay tuned for more updates from VinFast as they continue to make waves in the automotive world with their ambitious and innovative approach to building cars that stand out from the crowd.